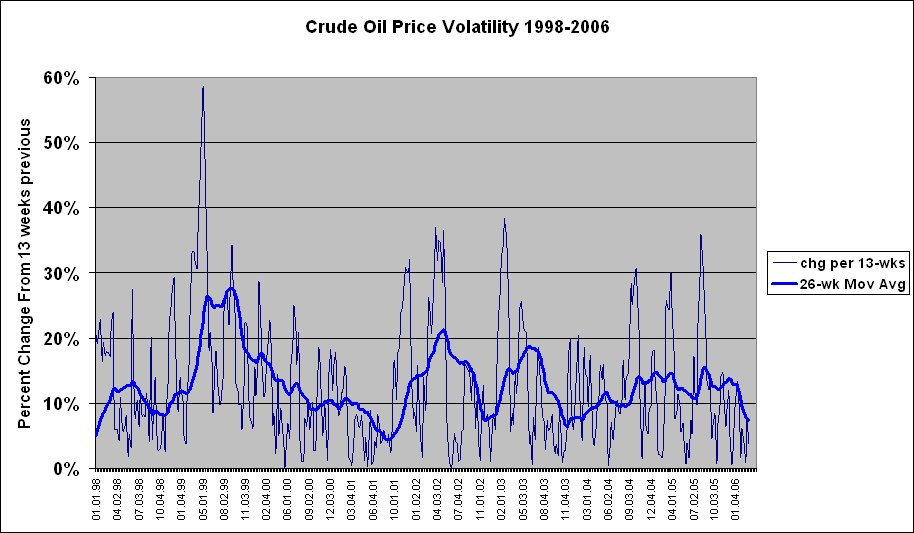

Oil Price Volatility 1998 - 2006

This uses a fairly crude method to calculate oil price volatility. I average the closing prices for Nymex futures each week. This becomes the weekly price. Then I compare the percentage difference between each week and the one 13 weeks before. I take the absolute value of this percentage change and then use a 26-week(6 month) simple moving average of number as an indicator of volatility. Not included in this version (to be added in future releases) is a trendline showing a slight downward trend over this specific period.

0 Comments:

Post a Comment

<< Home